Instant town on drawing board

Randy Shore

Sun

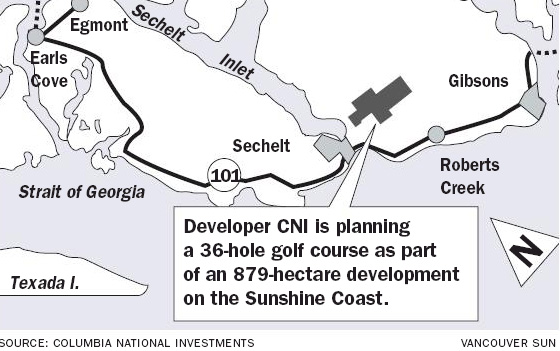

Columbia National Investments hopes to build a 36-hole golf course and resort village on the Dakota Ridge/Sechelt benchland

Real estate developer Columbia National Investments is planning to build a Whistler-style resort on raw land near Sechelt, using recently tweaked provincial legislation to create an instant town with municipal powers for taxation and public services.

The centrepiece of the community is to be a 36-hole golf course surrounded by view homes, hotels and condominiums with a village and retail development.

Bill 11, passed last month, allows the provincial cabinet to create “instant” municipalities in rural areas to promote resort development and grants special powers to resort communities to provide fire, sewerage and water services as well as facilitate special taxation powers and group marketing.

“The resort municipality legislation is going to allow us to build a resort on that hill,” said Steve Dunton, CEO of Abbotsford-based Columbia National. He says the proximity of the Dakota Ridge ski area qualifies CNI’s project for the powers described in the legislation, which he says gives the government considerable discretion in the kinds of resorts it approves.

“We just happen to have lands that fit right in,” Dunton said. “We should be able to move right ahead with our own resort municipality.”

According to a guide to the Mountain Resort Associations Act published last year by the Ministry of Community Services, the special municipal powers granted to Whistler under the Resort Municipality of Whistler Act of 1975 were a key element of the success of that resort, a record the government wants to duplicate.

Dunton says preliminary meetings with government officials have been positive. Solicitor-General John Les confirmed that, acting as Dunton’s MLA, he organized a meeting between CNI and Agriculture and Lands Minister Pat Bell earlier this year.

Premier Gordon Campbell announced in 2004 sweeping plans to double tourism revenue in B.C by 2015 by encouraging new investment in tourism infrastructure. Creating new resort municipalities is part of that effort.

Still in the early stages of development, Dakota Ridge offers cross-country skiing, snowshoeing and tobogganing in the winter, hiking, mountain biking and ATV and motorcycle trails in the summer.

The new legislation is a framework that paves the way for remote communities to develop resort infrastructure without troubling the legislature to pass new enabling law as was the case with Whistler, said ministry spokeswoman Anne McKinnon. The law is geared toward creating “instant towns” to develop alpine resorts in sparsely populated areas where there are few other economic drivers, she said. In the absence of those factors, proponents of resort developments are expected to work with local governments, she said.

“I told the [Sunshine Coast Regional District] to have a close look at this legislation,” said Powell River-Sunshine Coast NDP MLA Nicholas Simons, “because I can foresee the impact of this legislation on the ability of local government to have any say in their area.”

“CNI seems to think that they don’t need to bother the good folks at the regional district any more about their plans,” said Simons, a New Democrat. “It seems to me there should be a process where the local people and government have some input, particularly since this land is in the watershed.”

The Sunshine Coast Regional District has asked the ministry of community services for details of the act and for guidance, according to Ed Steeves, chairman of the SCRD and representative for the district of Sechelt. The board is concerned that CNI may be able to use the legislation to bypass the SCRD’s authority over development in the region.

“We have heard a proposal for such a development from CNI, but no plans or drawings,” Steeves said. “We are waiting for those.”

Steeves said he is aware that CNI is clearing the property and that they have recently acquired a gravel mining permit. But he said any further development of the land would face serious challenges securing a supply of water and disposing of sewage.

CNI is flying in American golf course designer Rees Jones for a helicopter tour of the 879-hectare (2,200-acre) property near Sechelt. A 36-hole golf course would require about 160 hectares (400 acres).

Jones has designed more than 100 golf courses, mainly in the U.S., and has remodelled dozens of others including the sites of seven U.S. Open venues, five PGA tour courses and three Ryder Cup courses.

“I want to give Rees the pick of the land for the golf course and then we will work around that,” said Dunton. “This is the canvas for a signature golf course.”

Jones said he looking forward to working with the ocean views in designing the course.

“With sandy soils and excellent local vegetation, it has the makings of a great golf experience,” Jones said. “Golf is a place where you escape the travails of life, so the isolation of this area makes it ideal.”

Columbia National purchased three major properties on the Sunshine Coast last year, the Sechelt bench lands near the Dakota Ridge winter recreation area, a 125-hectare parcel near Port Mellon and a 325-hectare property at McNabb Creek at a total price of $32 million.

CNI has logged about 80 hectares (200 acres) of the parcel to date with most of the wood going to the Port Mellon mill, Dunton said.

© The Vancouver Sun 2007