Sue Kirchhoff and Barbara Hagenbaugh

USA Today

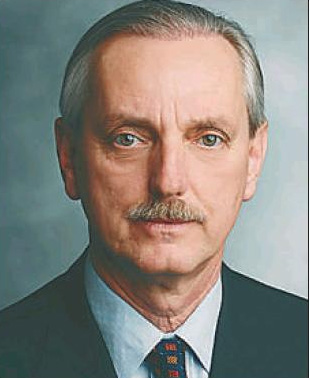

President Bush on Monday with, from left, SEC head Christopher Cox, Treasury chief Henry Paulson and Fed Chairman Ben Bernanke.

A home for sale in Antioch, Calif. With mortgage delinquency rates at 6%, investors and lenders with ties to housing have been hit hard.

WASHINGTON — The Federal Reserve is taking unprecedented steps as it battles a full-blown financial crisis: invoking rarely used legal authority to lend directly to investment banks, helping finance the bargain-basement sale of Bear Stearns to JPMorgan Chase and making the steepest interest-rate cuts in its modern history.

As the Fed meets Tuesday to consider another deep cut in the short-term lending rate that influences a broad swath of consumer and business loans, concern is growing that even its most aggressive efforts may not be enough to ease an unprecedented global credit crunch and keep the U.S. economy and world financial system on track.

Ken Rogoff, former chief economist for the International Monetary Fund and now an economics professor at Harvard University, says the Fed can address problems of liquidity — the ready availability of money. But, in this case, the problems are more complicated.

Rogoff predicts the issue ultimately will end up in the laps of Congress and the president.

“It’s a very delicate moment. The Fed can’t handle the situation at this point,” Rogoff said.

Despite aggressive Fed action, turmoil continues in financial markets. A growing number of economists say the country is already in a recession. Consumers, the main drivers of the economy, are cutting back their spending, and employers shed 63,000 jobs in February. On Monday, the Fed reported that U.S. factories were running at the slowest pace since October 2005.

“We are in uncharted territory,” says Kim Rupert, managing director of fixed income analysis at Action Economics. “We’ve all had a big learning experience in what the Fed can do. They have been creative in a lot of their solutions, but they still haven’t managed to stem the tide.”

The problem with homes

At the heart of the problem: a more than 20% decline in home construction and sales, falling prices and the fact that nearly 6% of home mortgages are now delinquent. That translates into a huge hit for investors and lenders holding mortgage-backed securities and related financial products. Compounding the situation, operations of investment banks like Bear Stearns were highly leveraged — using borrowed money. As the firms incur losses, they are forced to pull back. And as lenders rein in activity, consumers and businesses have a tough time securing even higher-cost loans.

So, even though the Fed has cut a key interest rate to 3% from 5.25% last September, market-based interest rates have not fallen as expected. That makes it hard for homeowners to refinance mortgages or businesses to expand, thereby reinforcing the downward spiral.

Goldman Sachs and other analysts recently predicted that losses from the housing debacle could reach $2 trillion or more.

This weekend’s jury-rigged sale of Bear Stearns for $2 a share — down from its share price of more than $30 last week — illustrates the extreme stresses on the system. That has helped spur a growing, if grudging, move by the White House and Congress toward stronger action to address underlying problems in the housing and financial markets.

On the political front

The economic pressures are leading to political pressures.

“One thing for certain is we’re in challenging times,” President Bush said at the White House on Monday, adding that his administration is closely monitoring the situation and is prepared to “act decisively, in a way that continues to bring order to the financial markets.”

Bush met with Fed chief Ben Bernanke, Treasury Secretary Henry Paulson and other economic officials Monday afternoon. Bush in February signed a $168 billion stimulus bill that provides special tax rebates to consumers and allows businesses to write off certain expenses.

Aside from that, the administration has largely relied on voluntary initiatives, including pushing lenders to restructure mortgage loans to help homeowners avoid foreclosure.

Senate Majority Leader Harry Reid, D-Nev., has promised consideration of a second stimulus package extending unemployment benefits, funding construction and other infrastructure projects and providing other aid. He criticized the White House on Monday for being willing to bail out large investment banks while doing little for homeowners facing foreclosure.

As credit markets began to seize up last August, Bernanke and other Fed officials struggled to settle on a consistent approach. The Fed approved interest-rate cuts, then held off making additional rate reductions. It made capital available to banks but cautioned it would not bail out institutions that made bad financial bets.

Fighting a battle on 2 fronts

Since December, when it became clear that credit and economic problems were deeper than it had anticipated, the Fed has mounted an all-out effort to ease credit conditions. Even its earlier critics praise its actions as innovative and well-targeted.

Bernanke and his colleagues have parted with tradition on two main fronts.

First, the Fed has developed new lending programs to help keep markets liquid, meaning that assets may be easily bought and sold. It has set up a special program with central banks around the world to auction funds to lenders. The Fed has offered to swap ultrasafe Treasury securities for mortgage-backed securities to provide needed capital to markets, and has liberalized the terms for banks borrowing from the discount window.

On a second front, the Fed has approved a series of steep cuts in the federal funds rate to aid the overall economy. The federal funds rate affects the interest that consumers pay, particularly on car loans, credit cards, home-equity lines of credit and the like.

“It’s sort of breathtaking the turmoil that we have seen in the credit markets. … This seems virtually unique,” says former San Francisco Fed president Robert Parry. “I’ve been really impressed that the Fed realizes that this is not a traditional case of economic weakness that (only) requires the traditional medicine of a reduction in rates.”

The central bank’s most recent moves underscore the trends. Faced with the possible bankruptcy of Bear Stearns, the nation’s fifth-largest investment bank, the Fed on Friday said it would provide financing to Bear Stearns, acting through JPMorgan Chase.

Over the weekend, officials from the Fed, the Treasury Department and Bear Stearns entered into a flurry of consultations about the situation. New York Fed Chairman Tim Geithner at times was juggling two calls at once. Bernanke, who normally works on Saturday and Sunday mornings even in calm times, settled in for the duration at Fed headquarters in Washington, D.C.

Late Sunday afternoon, the Fed Board of Governors by a 5-0 vote approved several measures to resolve the Bear Stearns crisis and address broader market issues.

• The Fed voted to cut the interest rate on direct loans to banks through its discount window to 3.25% from 3.5% and to extend the loans to 90 days from 30 days.

• The central bank voted to invoke little-used legal authority letting it lend to non-banks in “unusual and exigent circumstances.” Under that authority, the Fed will lend to a select group of about 20 securities dealers, including such venerable institutions as Goldman Sachs, to quickly get needed cash to the securities market. The firms will put up market-grade securities as collateral for overnight loans, including some mortgage-backed securities.

National City chief economist Richard DeKaser called the Fed’s move “absolutely the right thing to do” in creating an avenue to quickly get money to those who need it.

Fed assumes risk in Bear Stearns deal

The Fed also agreed to back $30 billion in financing to facilitate the sale of Bear Stearns to JPMorgan Chase. In doing so, the central bank assumed the risk for the collateral put up by Bear Stearns.

Allan Meltzer, an expert on the central bank at Carnegie Mellon University, praised the market-based moves, and said the central bank effectively let Bear Stearns fail.

“The only part of the bailout is the fact that they assumed $30 billion worth of risk,” Meltzer said.

The Fed isn’t done yet. The central bank is expected to approve another deep interest rate cut at a regularly scheduled meeting Tuesday.

Interest rate expectations put Fed in a bind

Economists and investors raised their earlier predictions for Fed interest rate action following the central bank’s move on Sunday. Fed policymakers are now widely expected to cut interest rates by a full percentage point, according to a market in which investors bet on future Fed moves. Such heightened expectations may be putting Fed policymakers in a bind: If they don’t cut their rate target to 2%, the lowest in more than three years, they risk a major stock sell-off.

“The point is, nobody even knows what the right amount is at this point,” says Joel Naroff, head of Naroff Economic Advisors.

Meltzer said while the Fed’s credit market policies are on target, its interest-rate policies are out of whack and risk spurring inflation.

Further, with the Fed cutting rates aggressively and other central banks, such as those in Europe, holding steady, the USA becomes less attractive as a place to invest. That has led to a sharp decline in the value of the dollar, which already is the lowest against a basket of major currencies since at least 1973, when exchange rates began floating.

“We faced some tough issues when I was there,” says former Richmond Fed president J. Alfred Broaddus. “But this is a tough process that they are going to have to go through at this meeting.”